Research Topics

Publications on Congressional Budget Office

-

Is the Link between Output and Jobs Broken?

Strategic Analysis, March 2013 | March 2013

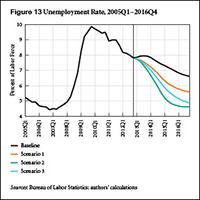

As this report goes to press, the official unemployment rate remains tragically elevated, compared even to rates at similar points in previous recoveries. The US economy seems once again to be in a “jobless recovery,” though the unemployment rate has been steadily declining for years. At the same time, fiscal austerity has arrived, with the implementation of the sequester cuts, following tax increases and the ending of emergency extended unemployment benefits just two months ago.

Our new report provides medium-term projections of employment and economic growth under four different scenarios. The baseline scenario starts by assuming the same growth rates and government deficits as the Congressional Budget Office’s (CBO) baseline projection from earlier this year. The result is a new surge of the unemployment rate to nearly 8 percent in the third quarter of this year, followed by a very gradual new recovery. Scenarios 1 and 2 seek to reach unemployment-rate goals of 6.5 percent and 5.5 percent, respectively, by the end of next year, using new fiscal stimulus.

We find in these simulations that reaching the goals requires large amounts of fiscal stimulus, compared to the CBO baseline. For example, in order to reach 5.5 percent unemployment in 2014, scenario 2 assumes 11 percent growth in inflation-adjusted government spending and transfers, along with lower taxes.

As an alternative, scenario 3 adds an extra increase to growth abroad and to private borrowing, along with the same amount of fiscal stimulus as in scenario 1. In this last scenario of the report, the unemployment rate finally pierces the 5.5 percent threshold from the previous scenario in the third quarter of 2015. We conclude with some thoughts about how such an increase in demand from all three sectors—government, private, and external—might be realistically obtained.

Download:Associated Program:Author(s):

-

Back to Business as Usual? Or a Fiscal Boost?

Strategic Analysis, April 2012 | April 2012Though the economy appears to be gradually gaining momentum, broad measures indicate that 14.5 percent of the US labor force is unemployed or underemployed, not much below the 16.2 percent rate reached a full year ago. In this new report in our Strategic Analysis series, we first discuss several slow-moving factors that make it difficult to achieve a full and sustainable economic recovery: the gradual redistribution of income toward the wealthiest 1 percent of households; a failure to fully stabilize and reregulate finance; serious fiscal troubles for state and local governments; and detritus from the financial crisis that remains on household and corporate balance sheets. These factors contribute to a situation in which employment has not risen fast enough since the (supposed) end of the recession to significantly increase the employment-population ratio. Meanwhile, public investment at all levels of government fell from roughly 3.7 percent of GDP in 2008 to 3.2 percent in the fourth quarter of 2011, helping to explain the weak economic picture.

For this report, we use the Levy Institute macro model to simulate the economy under the following three scenarios: (1) a private borrowing scenario, in which we find the appropriate amount of private sector net borrowing/lending to achieve the path of employment growth projected under current policies by the Congressional Budget Office (CBO), in a report characterized by excessive optimism and a bias toward deficit reduction; (2) a more plausible scenario, in which we assume that the federal government extends certain key tax cuts and that household borrowing increases at a more reasonable rate than in the previous scenario; and (3) a fiscal stimulus scenario, in which we simulate the effects of a fully “paid for” 1 percent increase in government investment.

The results show the importance of debt accumulation as a consideration in macro policymaking. The first scenario reproduces the CBO’s relatively optimistic employment projections, but our results indicate that this private-sector-led growth scenario quickly brings household and business debt to new all-time highs as percentages of GDP. We note that the CBO makes its projections using an orthodox model with several common, but fundamental, flaws. This makes possible the agency’s result that current policies will reduce the unemployment rate without a run-up in the private sector’s debt—“business as usual,” in the words of our report’s title.

The policies weighed in the second scenario do not perform much better, despite a looser fiscal stance. Finally, our third scenario illustrates that a small, tax-financed increase in government investment could lower the unemployment rate significantly—by about one-half of 1 percent. A stimulus package of this size might be within the realm of political possibility at this juncture. However, our results lead us to surmise that it would take a much more substantial fiscal stimulus to reduce unemployment to a level that most policymakers would regard as acceptable.

Download:Associated Program:Author(s): -

Is the Recovery Sustainable?

Strategic Analysis, December 2011 | December 2011Fiscal austerity is now a worldwide phenomenon, and the global growth slowdown is highly unfavorable for policymakers at the national level. According to our Macro Modeling Team's baseline forecast, fears of prolonged stagnation and a moribund employment market are well justified. Assuming no change in the value of the dollar or interest rates, and deficit levels consistent with the Congressional Budget Office’s most recent “no-change” scenario, growth will remain very weak through 2016 and unemployment will exceed 9 percent.

In an alternate scenario, the authors simulate the effect of new austerity measures that are commensurate with the implementation of large federal budget cuts. Here, growth falls to 0.06 percent in the second quarter of 2014 before leveling off at approximately 1 percent and unemployment rises to 10.7 percent by the end of 2016. In their fiscal stimulus scenario, real GDP growth increases very quickly, unemployment declines to 7.2 percent, and the US current account balance reaches 1.9 percent by the end of 2016—with a debt-to-GDP ratio that, at 97.4 percent, is only slightly higher than in the baseline scenario.

An export-led growth strategy may accomplish little more than drawing a small number of scarce customers away from other exporting nations, and the authors expect no net contribution to aggregate demand growth from the financial sector. A further fiscal stimulus is clearly in order, they say, but an ill-timed round of fiscal austerity could result in a perilous situation for Washington.

Download:Associated Program:Author(s): -

Is the Federal Debt Unsustainable?

Policy Note 2011/2 | May 2011By general agreement, the federal budget is on an “unsustainable path.” Try typing the phrase into Google News: 19 of the first 20 hits refer to the federal debt. But what does this actually mean? One suspects that some who use the phrase are guided by vague fears, or even that they don’t quite know what to be afraid of. Some people fear that there may come a moment when the government’s bond markets would close, forcing a default or “bankruptcy.” But the government controls the legal-tender currency in which its bonds are issued and can always pay its bills with cash. A more plausible worry is inflation—notably, the threat of rising energy prices in an oil-short world—alongside depreciation of the dollar, either of which would reduce the real return on government bonds. But neither oil-price inflation nor dollar devaluation constitutes default, and neither would be intrinsically “unsustainable.”

After a brief discussion of the major worries, Senior Scholar James Galbraith focuses on one, and only one, critical issue: the actual behavior of the public-debt-to-GDP ratio under differing economic assumptions through time. His conclusion? The CBO’s assumption that the United States must offer a real interest rate on the public debt higher than the real growth rate by itself creates an unsustainability that is not otherwise there. Changing that one assumption completely alters the long-term dynamic of the public debt. By the terms of the CBO’s own model, a low interest rate erases the notion that the US debt-to-GDP ratio is on an “unsustainable path.” The prudent policy conclusion? Keep the projected interest rate down. Otherwise, stay cool: don’t change the expected primary deficit abruptly, and allow the economy to recover through time.

Download:Associated Program:Author(s): -

Jobless Recovery Is No Recovery: Prospects for the US Economy

Strategic Analysis, March 2011 | March 2011The US economy grew reasonably fast during the last quarter of 2010, and the general expectation is that satisfactory growth will continue in 2011–12. The expansion may, indeed, continue into 2013. But with large deficits in both the government and foreign sectors, satisfactory growth in the medium term cannot be achieved without a major, sustained increase in net export demand. This, of course, cannot happen without either a cut in the domestic absorption of US goods and services or a revaluation of the currencies of the major US trading partners.

Our policy message is fairly simple, and one that events over the years have tended to vindicate. Most observers have argued for reductions in government borrowing, but few have pointed out the potential instabilities that could arise from a growth strategy based largely on private borrowing—as the recent financial crisis has shown. With the economy operating at far less than full employment, we think Americans will ultimately have to grit their teeth for some hair-raising deficit figures, but they should take heart in recent data showing record-low “core” CPI inflation—and the potential for export-led growth to begin reducing unemployment.

Download:Associated Program:Author(s):