Research Topics

Publications on Aggregate demand

-

The Aggregate Production Function and Solow’s “Three Denials”

Working Paper No. 1046 | March 2024This paper offers a retrospective view of the key pillar of Solow’s neoclassical growth model, namely the aggregate production function. We review how this tool came to life and how it has survived until today, despite three criticisms that undermined its raison d’être. They are the Cambridge Capital Theory Controversies, the Aggregation Problem, and the Accounting Identity. These criticisms were forgotten by the profession, not because they were wrong but because of the key role played by Robert Solow in the field. Today, these criticisms are not even mentioned when students are introduced to (neoclassical) growth theory, which is presented in most economics departments and macroeconomics textbooks as the only theory worth studying.

-

Distribution and Gender Effects on the Path of Economic Growth

Working Paper No. 959 | June 2020Comparative Evidence for Developed, Semi-Industrialized, and Low-Income Agricultural Economies

This paper applies a robust empirical methodology, which considers issues relating to cross-country heterogeneity and cross-sectional dependence, to inspect the contributions of gender equality and factor income distribution to an economy’s growth path. A dynamic model of aggregate demand is estimated on a unique panel dataset from 46 countries that are further grouped into developed (DC), semi-industrialized (SIEs), and low-income agricultural economies (LIAEs).

The empirical findings suggest that, overall, growth is driven by investment in the short run and domestic demand in the long run. In the short run, the results suggest that low female wages act as a stimulus to growth in SIEs but may promote contractionary pressures on demand in the long run. For LIAEs and DCs, the effect of improved labor market conditions for women—leaving men’s constant—on demand-led growth conditions are positive in the short run but may harm long-term growth prospects.

In all, the empirical evidence, combined with the stylized facts about institutional and economic inequality, suggests that the impact of gender and income inequality on macroeconomic outcomes will differ depending on the economic structure and level of economic development.Download:Associated Program:Author(s):Ruth Badru -

A Simple Model of Income, Aggregate Demand, and the Process of Credit Creation by Private Banks

Working Paper No. 777 | October 2013This paper presents a small macroeconomic model describing the main mechanisms of the process of credit creation by the private banking system. The model is composed of a core unit—where the dynamics of income, credit, and aggregate demand are determined—and a set of sectoral accounts that ensure its stock-flow consistency. In order to grasp the role of credit and banks in the functioning of the economic system, we make an explicit distinction between planned and realized variables, thanks to which, while maintaining the ex-post accounting consistency, we are able to introduce an ex-ante wedge between current aggregate income and planned expenditure. Private banks are the only economic agents capable of filling this gap through the creation of new credit. Through the use of numerical simulation, we discuss the link between credit creation and the expansion of economic activity, also contributing to a recent academic debate on the relation between income, debt, and aggregate demand.

Download:Associated Program:Author(s):Giovanni Bernardo Emanuele Campiglio -

Reorienting Fiscal Policy

Working Paper No. 772 | August 2013A Critical Assessment of Fiscal Fine-Tuning

The present paper offers a fundamental critique of fiscal policy as it is understood in theory and exercised in practice. Two specific demand-side stabilization methods are examined here: conventional pump priming and the new designation of fiscal policy effectiveness found in the New Consensus literature. A theoretical critique of their respective transmission mechanisms reveals that they operate in a trickle-down fashion that not only fails to secure and maintain full employment but also contributes to the increasing postwar labor market precariousness and the erosion of income equality. The two conventional demand-side measures are then contrasted with the proposed alternative—a bottom-up approach to fiscal policy based on a reinterpretation of Keynes’s original policy prescriptions for full employment. The paper offers a theoretical, methodological, and policy rationale for government intervention that includes specific direct-employment and investment initiatives, which are inherently different from contemporary hydraulic fine-tuning measures. It outlines the contours of the modern bottom-up approach and concludes with some of its advantages over conventional stabilization methods.

Download:Associated Program:Author(s): -

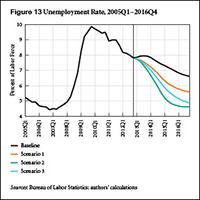

Is the Link between Output and Jobs Broken?

Strategic Analysis, March 2013 | March 2013

As this report goes to press, the official unemployment rate remains tragically elevated, compared even to rates at similar points in previous recoveries. The US economy seems once again to be in a “jobless recovery,” though the unemployment rate has been steadily declining for years. At the same time, fiscal austerity has arrived, with the implementation of the sequester cuts, following tax increases and the ending of emergency extended unemployment benefits just two months ago.

Our new report provides medium-term projections of employment and economic growth under four different scenarios. The baseline scenario starts by assuming the same growth rates and government deficits as the Congressional Budget Office’s (CBO) baseline projection from earlier this year. The result is a new surge of the unemployment rate to nearly 8 percent in the third quarter of this year, followed by a very gradual new recovery. Scenarios 1 and 2 seek to reach unemployment-rate goals of 6.5 percent and 5.5 percent, respectively, by the end of next year, using new fiscal stimulus.

We find in these simulations that reaching the goals requires large amounts of fiscal stimulus, compared to the CBO baseline. For example, in order to reach 5.5 percent unemployment in 2014, scenario 2 assumes 11 percent growth in inflation-adjusted government spending and transfers, along with lower taxes.

As an alternative, scenario 3 adds an extra increase to growth abroad and to private borrowing, along with the same amount of fiscal stimulus as in scenario 1. In this last scenario of the report, the unemployment rate finally pierces the 5.5 percent threshold from the previous scenario in the third quarter of 2015. We conclude with some thoughts about how such an increase in demand from all three sectors—government, private, and external—might be realistically obtained.

Download:Associated Program:Author(s): -

Inequality and Household Finance during the Consumer Age

Working Paper No. 752 | February 2013One might expect that rising US income inequality would reduce demand growth and create a drag on the economy because higher-income groups spend a smaller share of income. But during a quarter century of rising inequality, US growth and employment were reasonably strong, by historical standards, until the Great Recession. This paper analyzes this paradox by disaggregating household spending, income, saving, and debt between the bottom 95 percent and top 5 percent of the income distribution. We find that the top 5 percent did indeed spend a smaller share of income, but demand drag did not occur because the spending share of the bottom 95 percent rose, accompanied by a historic increase in borrowing. The unsustainable rise in household leverage concentrated in the bottom 95 percent ultimately spawned the Great Recession. The demand drag of rising inequality could be one explanation for the stagnant recovery in the recession’s aftermath.

-

Debtors’ Crisis or Creditors’ Crisis?

Public Policy Brief No. 121, 2011 | November 2011Who Pays for the European Sovereign and Subprime Mortgage Losses?

In the context of the eurozone’s sovereign debt crisis and the US subprime mortgage crisis, Senior Scholar Jan Kregel looks at the question of how we ought to distribute losses between borrowers and lenders in cases of debt resolution. Kregel tackles a prominent approach to this question that is grounded in an analysis of individual action and behavioral characteristics, an approach that tends toward the conclusion that the borrower should be responsible for making creditors whole. The presumption behind this style of analysis is that the borrower—the purportedly deceitful subprime mortgagee or supposedly profligate Greek—is the cause of the loss, and therefore should bear the entire burden.

Download:Associated Program:Author(s):Jan Kregel